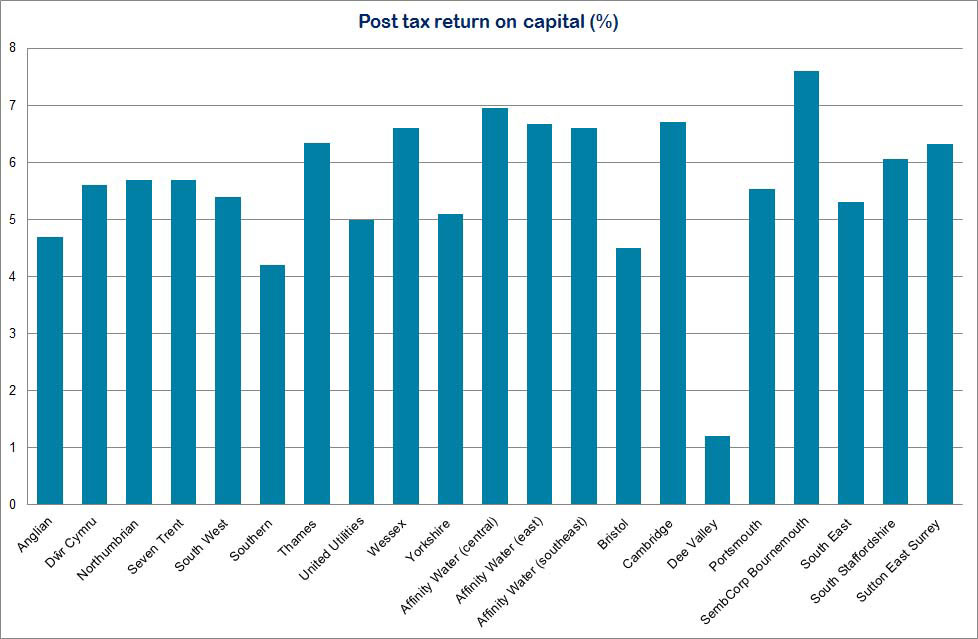

Post-tax return on capital

This is the return (required by providers of finance) on company assets as a proportion of the regulatory capital value (RCV). This is calculated as operating profit (a measure of income that tells investors how much revenue will eventually become profit), less tax, divided by the RCV. It is expressed in percentage terms.

It is used as a proxy for comparison against a company’s performance relative to the cost of capital in price limits. At the 2009 price review, the expected return on capital in price limits was 5.1% for all Water and Sewerage Companies (WaSCs), 5.3% for Veolia Central (now Affinity Water) and South East Water and 5.5% for all other water only companies (WoCs).

Credit rating

Just like an individual has a credit rating to obtain a mortgage or a loan from a bank, so do companies. Investors use these credit ratings to assess a company’s credit worthiness, that is how risky is it to lend this company money.

The lower the rating the higher the risk and vice versa. If a company has a high credit rating its rate of interest repayments will be lower and if a company has a low credit rating its rate of interest payments will be higher. The three main credit rating agencies that provide ratings for companies and government debts are Moody’s, Standard and Poor’s and Fitch Ratings.

Not all companies have credit ratings.

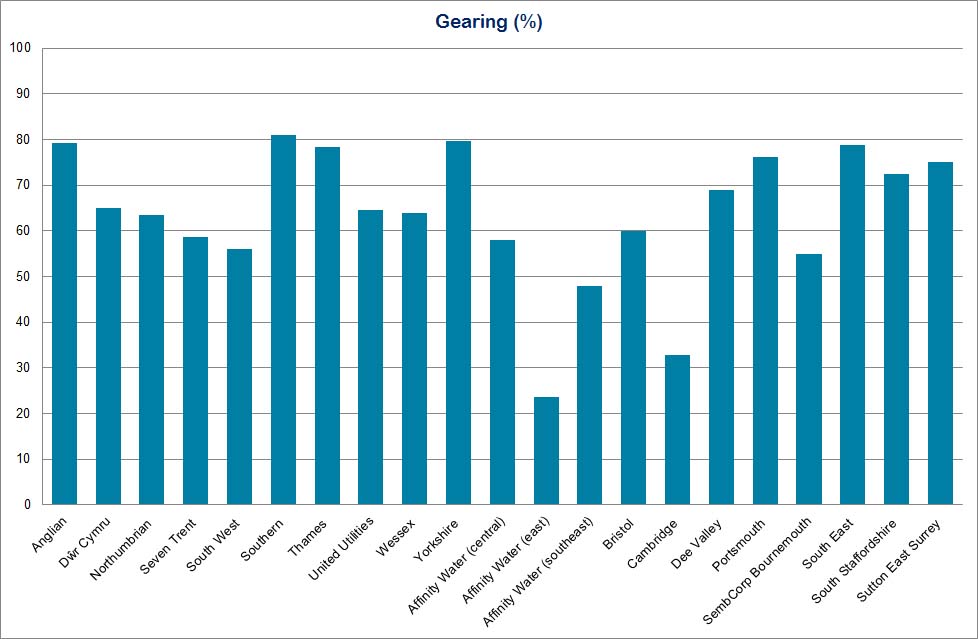

Gearing

Gearing shows how much debt a company has as a proportion of its regulatory capital base. It is generally a percentage and measured as net debt (total debt less any cash) divided by the regulatory capital value. Having high levels of debt can be viewed as having higher financial risk since companies’ must avoid defaulting on the loan. Conversely, payments to equity, that is dividends to shareholders, do not have to be be made, and it is at the discretion of the company whether these are paid at all. Gearing is a measure which credit rating agencies also look at in assessing the overall level of risk a company is exposed to.

Interest cover

This measure assesses how many times a company is able to pay necessary interest charges out of its profits after it has paid its other costs. The higher the number the more comfortable the company is able pay interest. Interest cover of 1.6 times is one measure financial agencies will consider when determining a company’s credit rating to be strong.

Data

| Return on regulatory capital value | Credit rating** | Gearing | Interest cover | |

|---|---|---|---|---|

| Anglian | 4.7% | Baa1 | 79% | 1.4 |

| Dŵr Cymru | 5.6% | A3 | 65% | 1.8 |

| Northumbrian | 5.7% | BBB+ | 64% | 1.9 |

| Severn Trent | 5.7% | BBB+ | 59% | 3.7 |

| South West | 5.4% | — | 56% | 2.1 |

| Southern | 4.2% | Baa2 | 81% | 1.6 |

| Thames | 6.3% | Baa1 | 78% | 1.4 |

| United Utilities | 5.0% | BBB+ | 65% | 2.0 |

| Wessex | 6.6% | BBB+ | 64% | 3.1 |

| Yorkshire | 5.1% | Baa1 | 80% | 1.4 |

| Affinity Water* (central) | 7.0% | BBB+ | 58% | 2.5 |

| Affinity Water* (east) | 6.7% | — | 24% | 2.7 |

| Affinity Water* (southeast) | 6.6% | — | 48% | 1.4 |

| Bristol | 4.5% | Baa1 | 60% | 1.6 |

| Cambridge | 6.7% | — | 33% | 4.7 |

| Dee Valley | 1.2% | — | 69% | 3.1 |

| Portsmouth | 5.5% | — | 76% | 1.9 |

| Sembcorp Bournemouth | 7.6% | — | 55% | 4.4 |

| South East | 5.3% | BBB | 79% | 2.3 |

| South Staffs | 6.1% | Baa2 | 72% | 2.8 |

| Sutton & East Surrey | 6.3% | BBB | 75% | 1.2 |

*Formerly Veolia Water Central, Veolia Water East and Veolia Water Southeast.

**Not all companies have a credit rating.

| Back to additional data about companies’ performance 2011-12 main page |